GO AD FREE | Get your Digital Subscription for only 50p a week! Use code SUMMER

GET STARTEDMore on KentOnline

GO AD FREE | Get your Digital Subscription for only 50p a week! Use code SUMMER

GET STARTEDMore on KentOnline

The current headlines about the threat of increasing interest rates can seem a little baffling and alarming. The big question most will be asking is: "Just how will it affect me?"

We take a look at the key issues and why - for both homeowners and those in the rental market - the current uncertainty is likely to, ultimately, be felt in our back pocket.

Is my mortgage set to increase? And, if so, when?

Not necessarily. At least not yet. It all depends on what sort of mortgage you have. If, for example, you agreed a five-year fixed term deal with your lender, and still have several years remaining, your payment is effectively locked in and you'll not need to pay any more. However, if your deal has less than 12 months to run, it may be worth having a look at your options.

Basically, if interest rates start climbing rapidly, so will every mortgage offer from the big lenders. However, if you move fast you may be able to lock in a deal before the rates are hiked again (and the fears are they will keep rising over the months to come).

Agree a deal in principle, and almost all lenders will give you a mortgage offer which lasts for six months which they will honour. It means you have time to see the direction of travel and whether it's worth taking it up within the six months.

It is, however, a gamble. If the rates keep increasing - which seems likely - interest rates may be significantly higher this time next year which would add even more to your monthly payment.

Mortgage advisors are also advising those within a year of their fixed rate expiring to weigh up paying a penalty to pull out of their agreed term early to lock in cheaper prices going forward.

Whether your deal is ending, or about to end, don't expect it to cost the same or any less. The historic low rates we've seen in recent years appear to be coming to an end - so if you took out a mortgage based on a low interest rate (it's been below 1% for more than 10 years) then today's rate of 2.5% will mean you are likely to be paying several hundred pounds more for a like-for-like repayment plan.

If, however, you have a tracker mortgage - which, as the name suggests, tracks the Bank of England base rate - then every time the rate rises you will see an up-tick on your payment. They have been great over recent years as the rate kept falling...but are worth looking at again, as they start to rise, if you want certainty over your monthly out-goings.

The best advice? Get some professional advice before making a decision.

So just how much more am I set to pay?

This will depend almost entirely on what steps the Bank of England decides to take in terms of raising the interest rate. But, as a rule, every time the interest rates goes up - even by a quarter of a percent - it will nudge up your repayments.

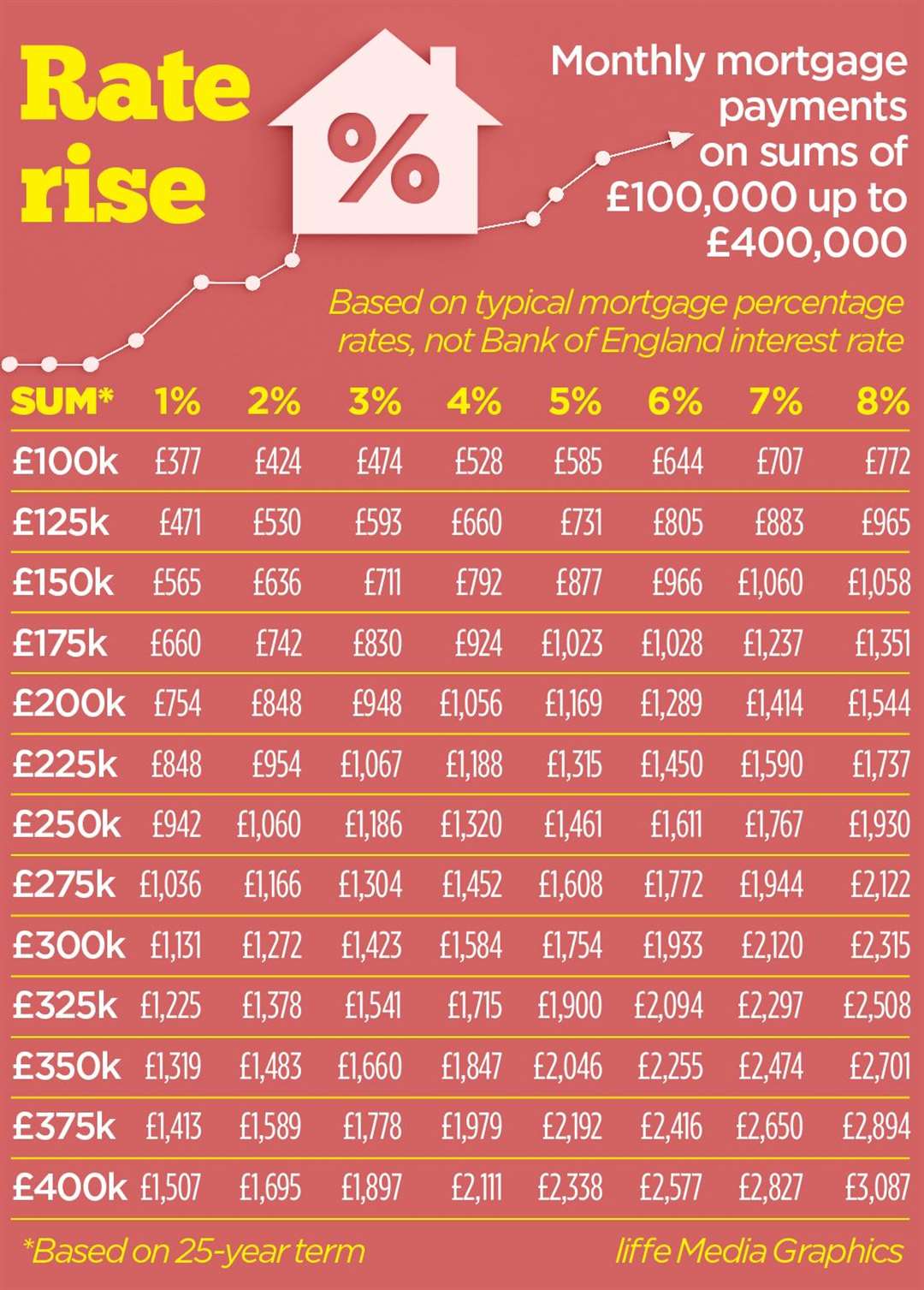

As an example, if you have a £200,000 mortgage over 25 years at an interest rate of 3% (bear in mind lenders' rates will always be higher than the Bank of England base rate), the monthly cost to you will be £946. If the interest rate nudges up just a quarter of a percent, you'll be paying £972. It may sound modest, but bear in mind lenders like Nationwide upped their rates by 1% overnight.

That rate is likely to keep going up for the next year at least. And sharply.

The table below gives you an indication of how a rise in the lenders' rates could send your monthly costs soaring.

Why are the interest rates expected to increase so much?

Interest rates are seen as a key method to control inflation. Inflation is, in its simplest terms, a measure by which the cost of goods increases.

Inflation is calculated by taking the average price of a range of goods and services we all use - ranging from groceries to fuel costs and much more besides - and comparing it month-on-month with the same price paid the year before.

Currently the inflation rate is 9.9%. Which means you're effectively paying 9.9% more for those same goods and service than you were in the corresponding month a year before.

The Bank of England is tasked by the Government to keep inflation at around 2% - a figure which is seen as the sign of a healthy, growing, economy, where the balance of wages and goods remains steady. Clearly things have got badly out of kilter.

This is caused by a host of issues but, more prominently, the shortage of various goods as a result of the global lockdowns during the pandemic. Scarcity drives prices up. And, of course, the war in Ukraine which has exacerbated already increasing energy prices.

The traditional method to slow down our spending - and thus reduce the rate of inflation - is by raising interest rates. This makes it more expensive to borrow money, increases our mortgages, and should slow things down.

The situation has been accelerated by last week's so-called 'mini-Budget' which rather flew in the face of attempts to bring inflation rates down.

Although energy price caps will reduce its rate of rise a little, by cutting taxes it puts more money in people's pockets which, in turn, encourages spending - the very thing the Bank of England is trying to limit.

Coupled with increased national borrowing to fund the cuts and the energy price cap, the markets have reacted with growing unease as investors now view the British pound as a less stable and reliable investment. Thus the price against the dollar - the standard comparison rate - fell to an all-time low earlier this week. Why does it matter to you? Well, a weakened pound against other currencies will increase prices as the pound doesn't carry the value it once did. Which, in turn, could fuel inflation.

Some analysts say interest rates could rise as much as 6% by next year. That would add hundreds of pounds onto mortgage payments for those not locked into long-term deals.

Could interest rates go down too?

Optimistically, if inflation is brought back under control - a situation unlikely to happen fast - the interest rates could be eased. But it's worth remembering that the last few years have seen unprecedented low interest rates.

On average, the UK interest rate between 1971 and 2022 averaged 7.15%. Which is rather more sobering. It hit an all-time high of 17% in November 1979 and a record low of 0.1% in March of 2020.

Given the uncertainties of recent years, it is almost impossible to predict how it will progress over the years ahead. But it would be wise to assume it will rise for at least the next year before, hopefully, stabilising.

Why are banks withdrawing mortgages?

Banks make good money from mortgages - money achieved by the interest rates they charge. These normally hover just above the Bank of England base rate. In short, it's their profit margins.

Following last week's mini-Budget and the response in the global financial markets - the pound's value plunged - it quickly became apparent interest rates would be set to rise.

The big bank lenders, therefore, became increasingly anxious at the start of the week that rates they offered today could be hiked, potentially quite significantly, within days, amid fears the Bank of England was about to announce an emergency interest rate rise.

As a precautionary measure, it pulled lots of its mortgage products. It has done so in order to allow it to gauge the direction of travel.

Until things become a little clearer, expect your options to be considerably limited for the time being at least. And then more expensive.

What happens if interest rate rises mean I cannot afford my mortgage?

These are unprecedented times. Already faced with a cost-of-living crisis, many will be anxious about interest rate rises pushing their major monthly cost - namely their mortgage - to a cost they will struggle to afford.

A rise in house repossessions - where the mortgage lender takes ownership of your property if you are unable to pay the monthly demands - seem inevitable. After all, the mortgage if effectively a loan secured against your property; failure to pay means the bank acquires your house.

They do so, however, only as a last resort.

It is why it is essential now that you are clear as to how you pay your mortgage and that you are ensuring you protect yourself as much as possible from the almost inevitable spiralling of interest rates. If in doubt, speak to your lender and discuss the situation.

Will it have an impact on house prices?

UK property prices have traditionally been relatively bullet proof. But increasing interest rates and economic uncertainty for the years ahead, could finally see them put in reverse.

Some analysts suggest they could plunge by at least 10% over the next 12 months as increased rates and the cost-of-living squeeze slow down demand and price properties - due to mortgage costs - out of the reach of many.

Does this have any impact on those who rent?

Inevitably, it will eventually have an impact on the rental market. The boom in buy-to-let mortgages over recent years was fuelled by the profit margin equation of low interest rates and increased demand for rental properties allowing a healthy monthly return.

If mortgage costs for landlords rise, they will look to pass those increases on. And that will, almost inevitably, be reflected in increased rents.